Banks, Busts and Bear Markets

What a difference a day can make! SVB was the ‘cool cat’ of the financial world, focused on technology, venture capital, and entrepreneurs. Following some bad investments in long-term bonds (We tried to warn them!), they eroded their capital reserves and were in the process of raising new money to plug the hole. Within a single working day, $42 billion[i] was withdrawn, wiping out the company and illustrating the speed at which panic can take hold in this new virtual world. Comparatively, Washington Mutual failed in 2008 when $16.7 billion was drawn over eight business days[ii]. For a fantastic breakdown into Silicon Valley’s Lightning Collapse, I invite you to read Preet Banerjee’s commentary (Link).

Similarly, Signature and Silvergate were heavily involved in crypto currency, a volatile sector facing its own headwinds at present, despite a very strong past few days. Credit-Suisse, by far the largest institution currently embroiled in this possible contagion, has not turned a profit in three years, and its revenues collapsed over the past 12 months, down to 33%[iii], before most investors had even heard of SVB. Management was so bad at Credit Suisse, that private investigators were hired to track executives at the bank in 2019[iv].

Heading into a recession, we feel that in the face of rising rates and more difficult economic conditions, we are only seeing the tip of the iceberg as it pertains to bad companies going under. Consider the following:

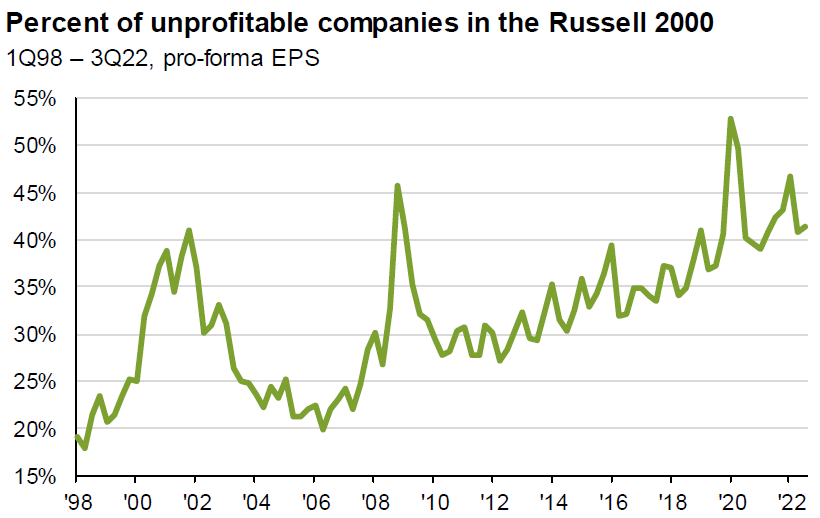

- 40% of companies on Russell 2000 were not profitable over the past three years[v]

- 13% of companies on S&P500 are zombie companies, and don’t produce enough profits to cover their interest obligation for three consecutive years[vi].

What happens to these companies when the economy turns, times get difficult, debts renew at higher rates, and banks shut their doors to high-risk borrowers?

The impact of these failures will be limited to shareholders and direct stakeholders in these businesses. The concern with the recent bank failures is that the damage might not be contained to just direct stakeholders, on account of the inter-connections in the banking system. In other words, there is a risk that well-run companies may also be destroyed due to a few bad actors.

In this special issue, we discuss the potential impacts on you as an investor.

Impact on Innova Pools

First and foremost, we have no direct exposure to SVB, Silvergate, Signature, First National, Credit Suisse, or any other bank caught up in this mess. At present, the Tactical Pool has a 43% exposure to the stock market and ~3% in banks, while the Growth Pool is closer to 75% stocks with less than 2% in banks. We expect that some of the private equity and venture capital investments held inside the pools may have some exposure to SVB given its prominence in Silicon Valley. Though impossible to determine at this point, we don’t foresee it resulting in a material impact on our investors given the US government’s guarantee on their deposits[i], and our relatively small exposure to this sector.[vii] .

As we have detailed in the past, we remain cautious in the Tactical Pool and prefer high quality companies with strong balance sheets, profit margins, and control on their debt. This strategy does not mean we will be immune to stock price movements, but rather that we should be less exposed to the absolute losses of capital that come with companies going bankrupt.

Some believe that success with investing in stocks mean avoiding the ups and downs of the market – as if this were a ‘bug’ rather than a ‘feature’ of the system. We believe that stock price movements are a feature that can’t be eliminated, and so we try to take advantage of it to the best of our ability through tactically increasing and decreasing exposure to stocks, and paying particularl attention to what matters over the long-run, profits!

Our increase in stocks over the past twelve months will likely translate to an increase in volatility over the next 6-12 as we enter the first real recession in over a decade. Along the way, we will be looking for discrepancies between stock price movements and what we view as the real value of companies – their profit-generating capacity.

Impact on Canadian Banks

So far, the contagion appears to be localized to US Regional Banks, with a sprinkling in the Eurozone to an already diseased Credit Suisse. It is imperative to understand the major differences between the US banking system and Canada’s. For starters, Canada counts 34 domestic banks[viii] while the US counts more than 4,000[ix]! Since 2001, 563 banks have failed in the US compared to 0 in Canada[x]. If we include the Great Depression in our time set, the number skyrockets to 9,000 failed banks in the United States[xi], compared to two small regional banks in Canada since 1923[xii].

We don’t believe there are serious concerns to the system wherein 92.6%[xiii] of total bank assets are held by the Big Six (RBC, TD, BNS, BMO, CIBC, and National, in that order)[xiv] all of which appear to be well-capitalized[xv],[xvi]. That said, they are not without risk – particularly those that are exceptionally exposed to higher-risk lending in the deflating real estate market, like Equitable Bank and Home Trust[xvii].

For depositors, both these institutions are covered by the CDIC which guarantees up to $100,000 per depositor against the bank’s default. The impact on the broader market should one of these institutions fail, would likely be an exacerbation of the real estate market’s drop as lending conditions would further constrict.

In short – we do not see any reasons that might prompt a run on Canadian Banks at present. Even so, we have been mindful to verify the deposit amounts per institution in order to try and mitigate any potential damage by spreading deposits across multiple accounts, respecting the $100,000 CDIC limit, where possible.

Impact on Tech Ecosystem

The largest impact we can foresee for the fallout of SVB, Silvergate, and Signature will be on the technology ecosystem within the US. All three of these banks were some of the friendliest lenders in tech, saying ‘Yes’ when others would balk, specifically with startups and entrepreneurs. And so – this leaves an important vacancy in the tech sector, one that won’t be as dramatically felt in the coming weeks, but rather in the coming months as many feel the pinch of their first real recession and turn to banks that aren’t quite as willing to advance cash to companies with no revenues or profits.

In summary – we don’t feel that the situation as it is currently understood, presents a clear and present danger to investors in our pools. That’s not to say that we aren’t expecting significant ups and downs in valuations over the coming months, but along with volatility comes opportunity.

We thank you for your continued trust in our stewardship and remain available to you to discuss the specifics of your accounts.

References

[i] https://edition.cnn.com/2023/03/14/tech/viral-bank-run/index.html#:~:text=Customers%20withdrew%20%2442%20billion%20in,said%20in%20a%20regulatory%20filing.

[ii] https://web.archive.org/web/20081001163230/http:/files.ots.treas.gov/730021.pdf

[iii] https://www.macrotrends.net/stocks/charts/CS/credit-suisse-group/net-income

[iv] https://www.theguardian.com/business/2019/dec/23/credit-suisse-admits-second-executive-was-followed-by-private-detectives

[v] https://am.jpmorgan.com/content/dam/jpm-am-aem/global/en/insights/market-insights/guide-to-the-markets/mi-guide-to-the-markets-us.pdf

[vi] https://www.bloomberg.com/news/articles/2022-05-31/america-s-zombie-firms-face-slow-death-as-easy-credit-era-ends

[vii] https://www.wsj.com/articles/joe-bidens-19-trillion-monday-svb-bailout-deposit-guarantee-fdic-fed-student-loan-too-big-to-fail-7e2de130

[viii] https://en.wikipedia.org/wiki/List_of_banks_and_credit_unions_in_Canada

[ix] https://en.wikipedia.org/wiki/List_of_largest_banks_in_the_United_States

[x] https://www.fdic.gov/bank/historical/bank/

[xi] https://digitalcommons.osgoode.yorku.ca/scholarly_works/1333

[xii] https://en.wikipedia.org/wiki/Banking_in_Canada

[xiii] https://www.advisor.ca/investments/market-insights/canadas-smaller-banks-face-higher-credit-risks-dbrs/

[xiv] https://www.investopedia.com/terms/b/bigfivebanks.asp

[xv] https://www.bankofcanada.ca/2022/05/staff-analytical-note-2022-5/

[xvi] https://www.ceicdata.com/en/indicator/canada/liquid-assets-ratio

[xvii] https://www.advisor.ca/investments/market-insights/canadas-smaller-banks-face-higher-credit-risks-dbrs/

- Hits: 9033