Bulls, Bears & Ballots

Bulls, Bears & Ballots: How the 2024 US Election Could Impact Your Investments

American voters are less than one week away from choosing their next leader. Elections matter for investors as even subtle policy changes can have a large impact on individual companies and the stock markets. This election cycle is significant to investors as it will determine how the next government intends to tackle America’s growing debt burden: by raising income, through taxes or tariffs, or through spending cuts.

Impact Harris

As might be expected, we believe that a Harris administration would likely result in a continuation of the Biden administration policies that are currently in place, to some degree. She has campaigned on increasing corporate tax rates, marginal rates for individuals earning over $400,000 per year, and a plan to introduce a ‘Billionaire tax’ that would set a minimum tax floor based on assets, not just income.

These measures may increase inflows to government coffers; however, an equal number of outflows have also been floated on the campaign trail, most notably, an expanded Child Tax Credit, increased Earned Income tax credit and assistance for first-time home buyers.

The expected net impact[i] of these promises does not translate to a balanced budget in the US, adding further pressure to US Debt loads. In addition, such a substantial increase to corporate tax rates would reduce net earnings per share, sending that already inflated metric stratospheric, potentially becoming the pinprick that bursts the bubble in US stocks.

Impact Trump

According to Trump's campaign promises, we can expect his team to extend the Tax Credits and Job Act (TCJA), established by his administration in 2017. According to some studies, fully extending the TCJA would reduce revenues by as much as $4.2 trillion over the next decade. Trump has campaigned for a universal tariff on all imported goods to the US to offset this shortfall. The Tax Foundation estimates that, if reciprocated by other countries, this would likely lead to a net drag on US output and net job creation, as well as surging inflation for the US consumer.

Former President Trump has also campaigned on a shift in US energy policy that would see an increased reliance on fossil fuels, attained through eliminating some environmental regulations that have delayed the development of pipelines and new capacity.

Fundamentally, we do not believe this plan supports long-term US or global growth and does not address the US debt situation meaningfully. We also believe this increases the likelihood of cross-border tensions, impoverishing the risk-to-reward relationship for stocks. Combined, this forces us to consider ‘risk off’ investments and to cherry-pick the companies that might be least impacted by these changes, including those that enjoy strong balance sheets and high-profit margins.

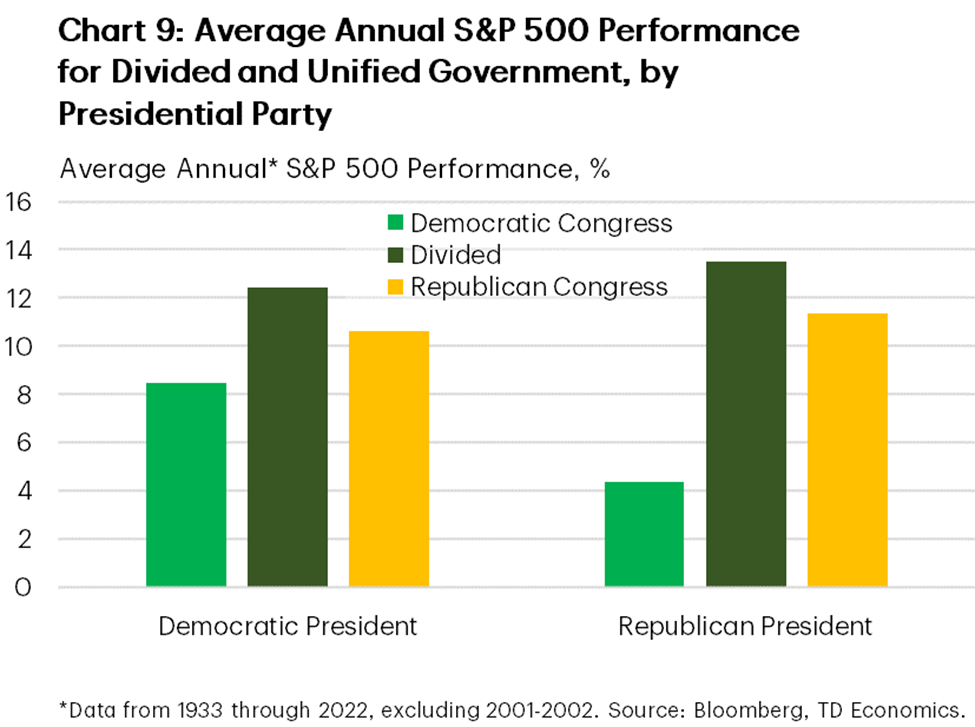

Impact Congress

The markets have historically performed very similarly whether Democrats or Republicans occupy the White House. Interestingly, the most significant divergence of returns occurs when the United States Congress is divided, as shown in the chart below:

Historically, a divided Congress has led to better investor outcomes, becoming the most critical historical guide for what to expect in the next four years.

Impact Unrest

Speaking of division, this iteration of ‘The Greatest Show on Earth’ has the potential to lead to unrest. With one of the parties already contesting early ballot entries, a repeat of the 2021 capitol attacks should be considered. Although we do not feel this presents a long-term risk to the United States, there is potential that this will lead to substantial short-term movements in the stock market.

What we are doing about it!

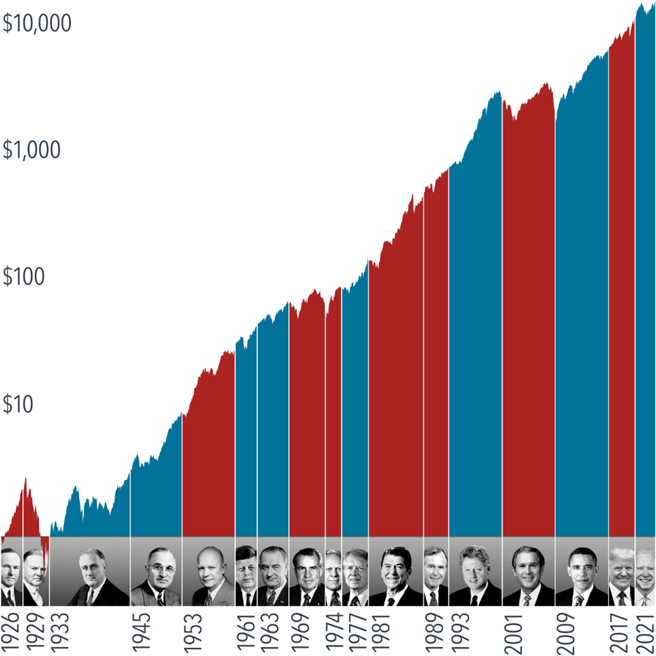

As we have been discussing with clients, the 2024 US election has been on our radar for many months. Historically speaking, the person who occupies the White House has little bearing on the upward march of the stock market, as shown by the following chart:

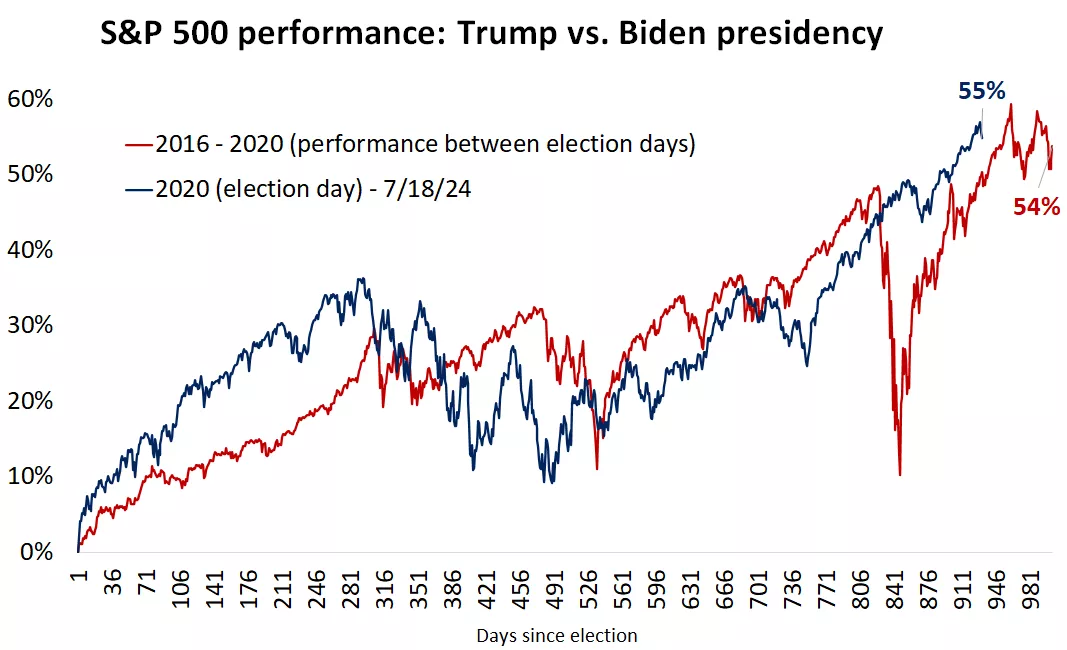

Despite all the rhetoric, even the most recent US presidencies have had very similar experiences on the stock market:

This is largely because regardless of the political party leading the country, Americans will shop at Costco, buy their medications, pay for their cell phone bills, and keep the economy moving. So long as the consumers keep spending, companies will make profits and share them with shareholders.

Therefore, we have not opted to do anything drastic with the portfolio. Instead, we have made minor changes to the portfolio that would hedge our positions if a contested election leads to increased market volatility. Specifically, we feel that such a scenario would undermine US debt, so we have reduced exposure in favour of commodities like gold and tangible assets like farmland and infrastructure.

Gold, in particular, has had an incredibly strong year-to-date primarily due to the uncertainty we see across global markets. Regular readers will recall that we generally bounce in and out of this position during times of maximum uncertainty rather than being long-term holders. This is because the stock market has historically generated almost 3 times that of gold over the long term [ii]. For that reason, we expect this allocation to be short-lived and directly related to our concerns over the US Treasuries market and potential unrest.

Summary

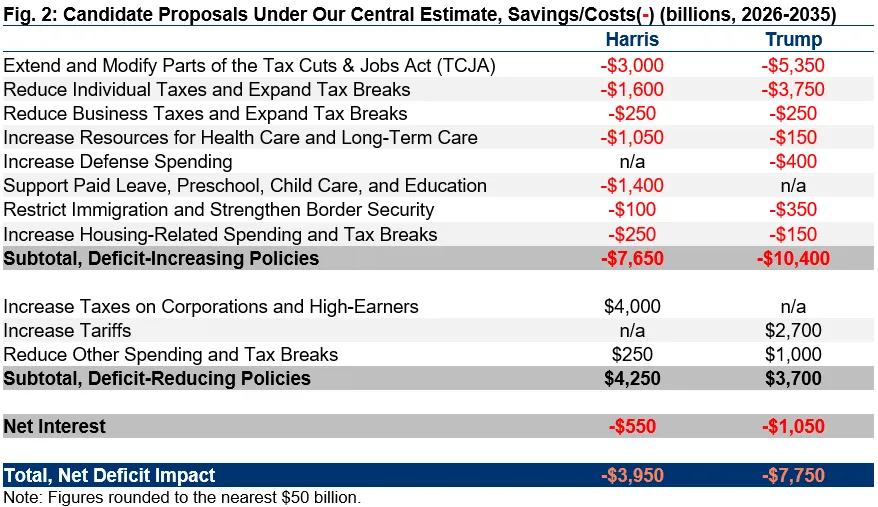

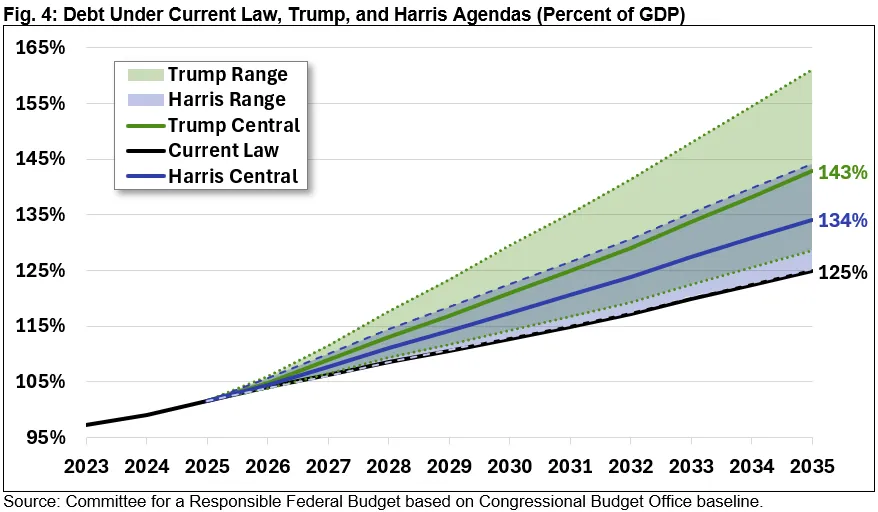

Like most pundits, we foresee a very tight race on all fronts. If 2016 taught us anything, it is that the margin of error with polls can change outcomes and that the popular vote is no longer needed to win control of the world’s most economically important country. As shown below, neither party’s platform seems to address the large deficits forecasted for the U.S., which we view as the most important threat to our client’s meeting their return objectives.

Therefore, we are preparing ourselves, and our portfolio, for volatility. We will monitor the situation closely and be ready to take advantage of opportunities as they present themselves.

Thank you for your continued trust in our stewardship.

[i] https://economics.td.com/ca-us-2024-election-econ-fin

[ii] https://www.investopedia.com/ask/answers/020915/has-gold-been-good-investment-over-long-term.asp

[iii] https://www.crfb.org/papers/fiscal-impact-harris-and-trump-campaign-plans

Jean-François Démoré is an advisor with Aligned Capital Partners Inc. (“ACPI”). The opinions expressed are those of the author and not necessarily those of ACPI. This material is provided for general information and the opinions expressed and information provided herein are subject to change without notice. Every effort has been made to compile this material from reliable sources however no warranty can be made as to its accuracy or completeness. Before acting on the information presented, please seek professional financial advice based on your personal circumstances. ACPI is a full-service investment dealer and a member of the Canadian Investor Protection Fund (“CIPF”) and the Canadian Investment Regulatory Organization (“CIRO”). Investment services are provided through Innova Wealth Management, an approved trade name of ACPI. Only investment-related products and services are offered through ACPI/Innova Wealth Management and covered by the CIPF.

- Hits: 6022